Following extensive deliberations, Congress has enacted comprehensive tax and spending legislation that President Trump signed into law on Independence Day, which is known as the “One Big Beautiful Bill” Act (or OBBBA). This sweeping budget encompasses numerous provisions, including the permanent extension of key Tax Cuts and Jobs Act components, enhanced state and local tax deduction limits, continued estate tax threshold expansions, and additional measures. The legislation seeks to balance these benefits through targeted spending reductions, particularly in areas like Medicaid funding.

The significance of this legislation extends beyond trade policy discussions that have dominated recent months, addressing the mounting uncertainty surrounding tax and spending policies that have persisted for years. Despite political divisions regarding the budget’s direction, the legislation eliminates the looming “tax cliff” scenario where substantial policy shifts could have occurred with the expiration of key provisions at year-end.

Taxation directly influences numerous financial planning considerations both for individuals and businesses. From a broader economic standpoint, investors remain concerned about government expenditure levels, expanding national debt, and related factors that have influenced market conditions over recent decades.

Given the multiple implications and changes both for individuals and businesses, here is a breakdown of the changes, including a comparison of prior tax law to the new OBBBA changes, as well as perspectives on who it may impact from a planning perspective.

Key Changes & Comparisons to Prior Tax Law

The OBBBA extends and enhances multiple key elements from the 2017 Tax Cuts and Jobs Act (TCJA) that faced expiration at year-end. Additionally, it incorporates new provisions offering taxpayer benefits, though these are only partially balanced by spending reductions elsewhere.

These modifications and others preserve the relatively favorable tax climate that has prevailed in recent decades. The accompanying charts above illustrate how current rates remain substantially below historical peaks from much of the 20th century, when top marginal rates surpassed 70% and occasionally exceeded 90% during wartime. The second chart above also shows the comparison of personal vs. business tax rates over those same periods as well.

Several of the major provisions include:

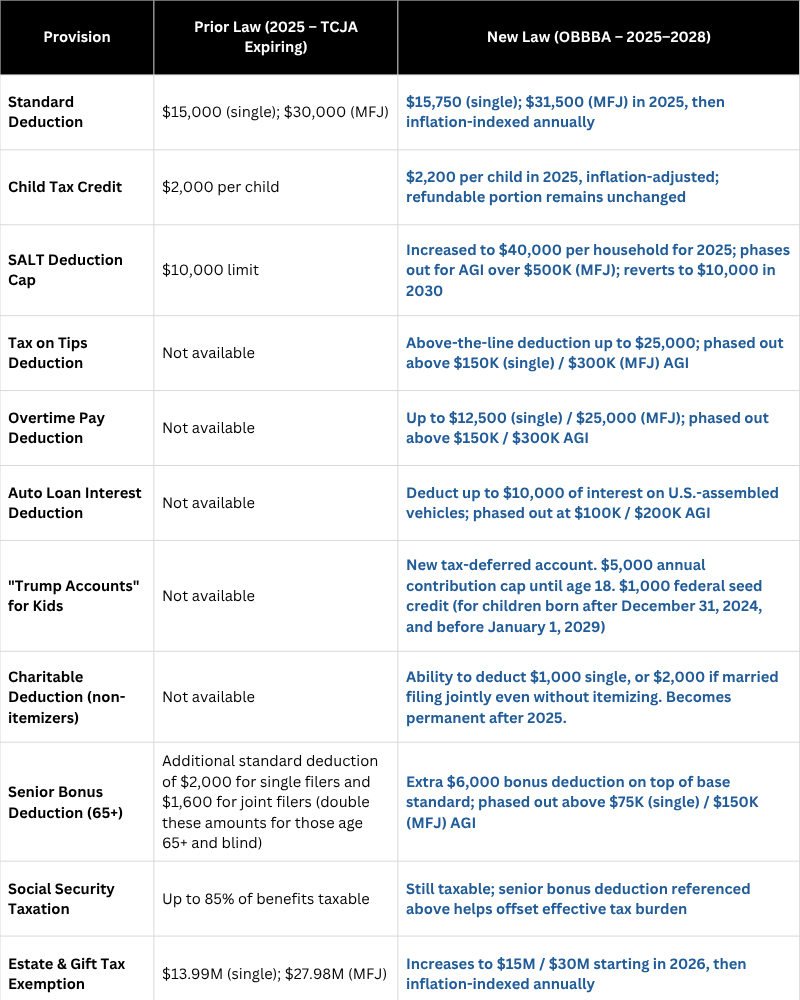

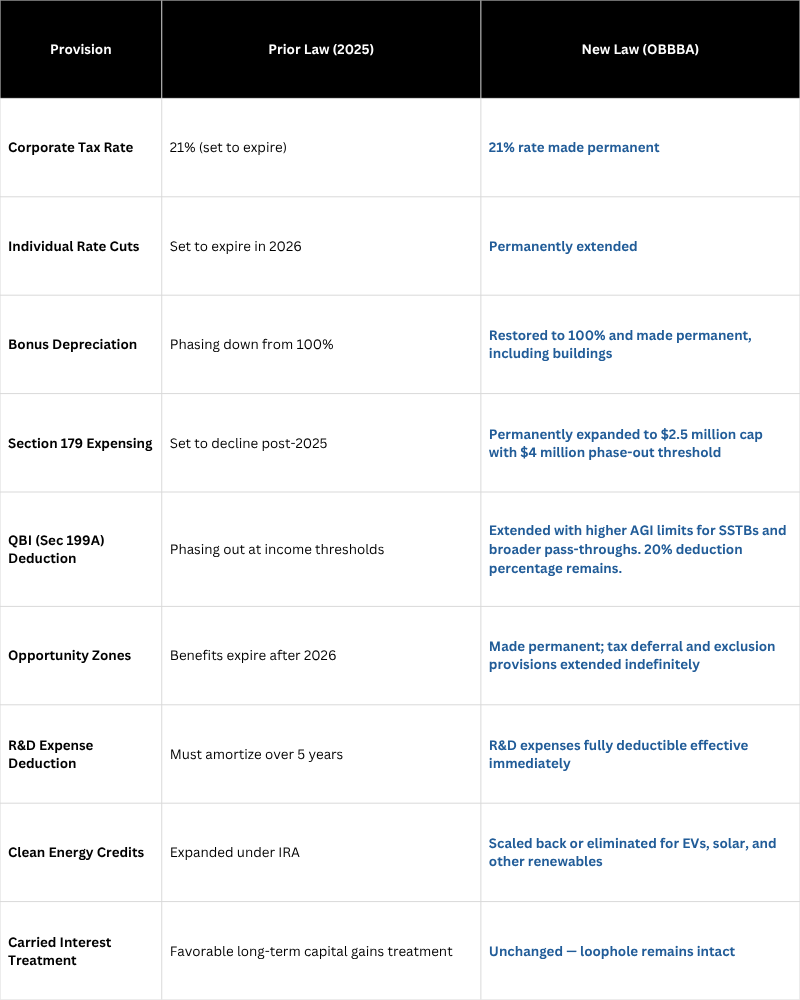

- TCJA tax rates and brackets receive permanent status, eliminating their original 2025 expiration date.

- Standard deduction amounts rise to $15,750 for individual filers and $31,500 for married filing jointly in 2025.

- Qualifying seniors receive an additional $6,000 deduction (often called a “senior bonus”) with phaseout beginning at $75,000 gross income. This provision sunsets in 2028.

- Alternative minimum tax exemption becomes permanent, with phaseout thresholds increasing to $500,000 for individual filers and future inflation indexing.

- Child tax credit expands from $2,000 to $2,200 per child, with inflation adjustments to preserve purchasing power over time.

- State and local tax (SALT) deduction cap rises to $40,000 from the previous $10,000 ceiling, including 1% annual increases through 2029 before reverting to $10,000 in 2030.

- Tip income deduction allows up to $25,000 annually for workers earning under $150,000, effective through 2028.

- Certain green energy tax credits face elimination, including electric vehicle and residential energy efficiency incentives.

- Federal debt ceiling increases by $5 trillion, removing near-term congressional debt limit debates and reducing political uncertainty.

- Business tax incentives expand to promote domestic investment and employment growth.

- Estate & Gift Tax Exemptions have been extended – increasing to $15 Million for individuals and $30 Million for married couples in 2026. The below chart shows historical estate tax exemption amounts and rates to illustrate their continued climb over the last 25+ years.

For comparison purposes, here are charts showing the key differences between prior tax law and OBBBA, both from personal and business tax perspectives:

Personal

Source: Internal Revenue Service (https://www.congress.gov/bill/119th-congress/house-bill/1/text)

Business

Source: Internal Revenue Service (https://www.congress.gov/bill/119th-congress/house-bill/1/text)

Impacts on Personal & Business Planning

Given these changes, there will be several different impacts on Americans depending on their situation. Some groups, both on the personal and business side, may be impacted more than others, including:

Individuals & Families

- Middle-income workers: Potential access to new deductions for tips, overtime, and auto loan interest.

- High-income earners & HNW families:

- Increased SALT cap may provide relief through 2028, especially those in high tax states

- Larger estate/gift exemption beginning in 2026 supports advanced legacy and gifting strategies

- Continued low marginal rates may enhance after-tax income

- Non-itemizers who give charitably: New above-the-line charitable deduction starting 2026

- Retirees 65+: Senior bonus deduction reduces effective tax rate on Social Security and other retirement income

- Many personal provisions expire after 2028

- SALT and deduction phase-outs may reduce access for higher AGI earners

- New charitable deduction for non-itemizers does not start until 2026

- Payroll taxes, Affordable Care Act surcharges, and capital gains rates remain unchanged

Businesses

- Small businesses and real estate investors:

- Permanent 21% corporate rate

- Expanded Section 179 expensing up to $2.5 million

- Bonus depreciation restored for equipment and buildings

- Pass-through entities:

- QBI deduction extended with more favorable phase-out thresholds

- Tech and manufacturing firms:

- Full expensing for R&D restores important innovation incentive

- Investors in underserved areas:

- Opportunity Zones made permanent – enables multiyear deferral/exclusion planning

Mounting fiscal deficit concerns

![]()

Switching gears, now let’s look at how the new legislation may impact the government deficit. Overall, tax policy and government deficits represent interconnected issues, as tax reductions diminish government revenues that must be balanced through reduced spending or additional borrowing. Nevertheless, most government expenditures support entitlement and defense programs that prove politically challenging to modify. Treasury Department data indicates that 2025 government spending allocates 21% to Social Security, 14% to Medicare, 13% to National Defense, and 14% to servicing existing national debt interest costs.

Consequently, government borrowing has grown consistently throughout the past century and will likely continue this trajectory. The Congressional Budget Office, a nonpartisan congressional support agency, projects that this new tax and spending legislation will contribute $3.4 trillion to national debt over the coming decade. This occurs against a federal debt backdrop already surpassing 120% of GDP, totaling $36.2 trillion, which represents approximately $106,000 per American citizen.

Regrettably, this challenge lacks straightforward solutions, particularly given its contentious political nature. Tax reductions can potentially stimulate economic growth, potentially offsetting revenue losses through enhanced economic activity. However, Washington’s historical record for budget balancing remains poor even during strong economic periods. The most recent balanced budgets occurred 25 years ago under the Clinton administration, with the previous occurrence 56 years earlier during the Johnson presidency.

The accompanying chart above demonstrates that individual income taxes now constitute the federal government’s primary revenue source. Social insurance taxes, or payroll taxes, are deducted from wages to fund Social Security, Medicare, unemployment insurance, and similar programs. Other revenue sources remain proportionally smaller, including corporate taxes reduced by the TCJA and excise taxes such as tariffs.

While tax policies certainly carry direct implications for investor financial plans and portfolios, their macroeconomic effects remain more constrained. Over extended periods, elevated debt levels may influence interest rates and inflation expectations. Although these factors have been relatively elevated recently, many worst-case scenarios have not materialized. Long-term investors should focus on maintaining diversified portfolios capable of performing across various fiscal and economic conditions, rather than responding solely to policy modifications.

Wrapping Things Up

While the deficit and increased government spending is of most concern, and bears watching (closely), the new tax legislation provides both certainty and potential planning opportunities. Largely, the new legislation extends the 2017 TCJA tax cuts with some new elements and nuances. The impact of the changes will depend on your specific situation, both on the personal and business side, so it is crucial to work with your tax professional and financial advisor.

Tax planning is a key component to our client services at Tenet. Now that the new tax law has been passed, we will be working closely with our clients to discuss how it may impact them specifically. If you have any questions, or would like to discuss potential impacts if you are not already a client, please don’t hesitate to contact us or schedule a time to meet with us.

Investment advisory services offered through Tenet Wealth Partners, LLC, a registered investment advisor with the U.S. Securities and Exchange Commission. This material is intended for informational purposes only. It should not be construed as legal or tax advice and is not intended to replace the advice of a qualified attorney or tax advisor. This information is not an offer or a solicitation to buy or sell securities. The information contained may have been compiled from third-party sources and is believed to be reliable.

The information provided in this communication was sourced by Tenet Wealth Partners through public information and public channels and is in no way proprietary to Tenet Wealth Partners, nor is the information provided Tenet Wealth Partner’s position, recommendation or investment advice. This material is provided for informational/educational purposes only. This material is not intended to constitute legal, tax, investment or financial advice. Investments are subject to risk, including but not limited to market and interest rate fluctuations.

Any performance data represents past performance which is no guarantee of future results. Prices/yields/figures mentioned herein are as of the date noted unless indicated otherwise. All figures subject to market fluctuation and change. Additional information available upon request.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

About The Author

Kevan Melchiorre, CFP®Co-Founder & Managing Partner

Kevan Melchiorre co-founded Tenet Wealth Partners in 2021 with a focus on delivering a premier client experience, supported by an innovative and fully integrated approach to wealth planning. As a CERTIFIED FINANCIAL PLANNER® practitioner with over 16 years of wealth management experience, Kevan partners with affluent individuals, families, and institutions to help align their capital […]

Learn more about Kevan